How to Make the Most of Your Savings in the New Tax Year

- Authors

-

-

- Name

- Patrick Maflin

-

As the tax year turned at the beginning of April, and with the cries of "Happy New Year" ringing around the Marine Accounts office, the thoughts of many have now turned towards what to do with their hard-earned savings from the year before.

Having undertaken consultation with an industry specialist financial advisor, we are pleased to present a short summary of some of your options.

Read on to find out how you can take advantage of tax breaks and government top ups, beyond the Seafarer’s Earnings Deduction (SED).

Chapters

- ISA (Individual Savings Account)

- What Are My Choices?

- Pensions

- Self-Invested Personal Pensions (SIPPs)

- Stakeholder Pensions

- Savings Beyond ISAs & Pensions

- Summary

ISA (Individual Savings Account)

With your employment income having reached your bank account without being touched by the taxman, the kind folk at HMRC are offering you even more opportunities to build your savings without having to pay them a penny.

Every year you can invest up to £20,000 in an ISA and any interest or gains will remain yours and yours alone.

Image source: https://www.pexels.com/photo/black-magnifying-gla...

What Are My Choices?

Cash ISA

This type of ISA is well known for being very low risk but, with historically low interest rates at present, they’re also likely to show little return as it stands currently.

Stocks & Shares ISA

A stocks & shares investment portfolio in which the gains will incur no tax liability.

Lifetime ISA

If you are between the ages of 18 and 40 you have the opportunity to invest up to £4000 per year with the government topping up whatever you put in by 20%.

Innovative Finance ISA

If you meet the stringent criteria applied to applicants, you can access this high-risk ISA in the hope that it will deliver high returns. Be careful here as your investment won’t be protected by the Financial Services Compensation Scheme (FSCS).

With 4 options to choose from varying in risk level, most investors will be able to find an account which will suit their needs.

Image source: https://www.pexels.com/photo/man-in-black-suit-ho...

Pensions

A pension is a financial instrument allowing you to squirrel away some of those hard-earned nuts for a time at which you are ready to retire.

Unlike many other industries, workplace pensions are not a standard feature of your employment so if you’d like to see a little more than the basic state pension in your bank account when you’re done working, it might be time to think about going private.

Pension investments receive favourable tax treatment and you may even find that the government is willing to top up some of your contributions for you.

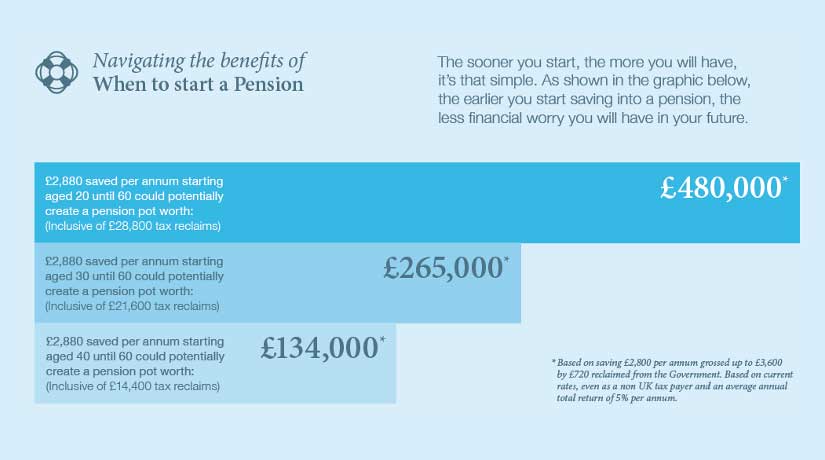

The graphic below shows your potential savings you could make by the age of 60 dependent on your current age:

Image source: https://www.tuvyc.com/media/1334/2008-lay-pension...

Self-Invested Personal Pensions (SIPPs)

The most common type of pension accounts held by crew are Self-Invested Personal Pensions (SIPPs); a UK government approved personal pensions scheme which you can access from the age of 55 under current rules.

SIPPs can offer much wider investment powers than may be available for other personal pensions and group personal pensions.

Most personal pensions are flexible and are portable.

If you change jobs or stop working, you may be able to continue contributing to the scheme, and if you join a new employer, you may be lucky enough to find that you can negotiate direct contributions from them before starting the job.

Stakeholder Pensions

Stakeholder Pensions are another common option taken up by crew and are well known for having limited charges and flexible contribution rates with a low minimum.

Your contributions are usually invested in a stocks & shares portfolios, with the manager looking to increase the value of your nest egg by the time you surrender the policy or withdraw your investment.

Whilst there is a prevalence in the use of the two types of pension scheme described above amongst yacht crew, there are a plethora of options available and a good financial advisor will be best placed to take you through what might best suit you.

Savings Beyond ISAs & Pensions

If you have savings over and above the thresholds for investment in ISAs and Pensions Schemes, you may now be wondering what you should do with the excess.

As per our earlier series of articles entitled The Rise of Bad Financial Advice, yacht crew are often encouraged to invest in complicated overseas or offshore investment schemes.

These can often incur high fees and show little return, with early surrender more often than not leaving you out of pocket, perhaps by many thousands of Euros.

Instead of being pulled in to this kind of policy, you may consider a regular stocks & shares portfolio.

This type of investment aims to offer a modest return with low fees; although it is important to bear in mind that, like most investments involving the stock market, the value could go down as well as up.

Summary

As described above there are many options available when it comes to establishing a tax efficient strategy to make the most of your savings, with the government happy to offer tax breaks and even top up your investment in some cases.

Whilst you may find that you have a good understanding of the type product that you are seeking, we would always advise that you contact a professional before moving forward.

A good, honest financial advisor will have many years of experience in navigating the system and may have some ideas which haven’t crossed your mind.

Consultations undertaken with Emma Parkes of Church House Investments

Disclaimer

Any advice in this publication is not intended or written by Marine Accounts to be used by a client or entity for the purpose of (i) avoiding penalties that may be imposed on any taxpayer or (ii) promoting, marketing or recommending to another party matters herein.

{kind=link}